Consumer Apps

This is Part 3 of the Consumer Demand Series.Introduction

Part 1: Merchant Front Office Apps - Setting the Foundation

Part 2: Creating Demand with Merchant Facing Apps

Part 3: Consumer Apps

Part 4: The Big Leap to Two-Sided Marketplace

In Part 1 of this series,I covered front office applications that help a merchant acquire and retain customers, and engage with them over time. In Part 2, I explored solutions to generate incremental demand for a merchant.

In this essay, I’ll discuss the role of consumer applications. To begin, I walk through the opportunity to land a wedge with the consumer in the form of a mobile app or consumer portal. These wedges typically are at the end of a VSV’s merchant workflow, to provide a consumer with strong utility or a better experience.

Take for example, Slice. Slice is a VSV for pizza shops that has a branded consumer app as a wedge with 9M+ active consumers; a front office to help their merchants drive demand; supplier extensions to leverage the collective scale of their 15K+ customers on key supplies such as pizza boxes and delivery rates; and even more services in the works. The consumer app allows them to funnel demand to their merchants, significantly enhancing their value. Everyone likes being able to sell more pies, though the Slice consumer app isn’t limited to pizza.

So why are consumer apps important to almost every VSV?

Direct Engagement

Consumer apps create a direct link between the VSV and the merchant’s customer. A consumer app gives the merchant (and the VSV) a communication channel and user information for future interactions. This stands in stark contrast with marketplaces, which will oftentimes obfuscate the consumer’s contact information from the merchant to force all interactions through their platform.

Owning the contact information allows for higher-value marketing campaigns to be built. The simplest version is just dropping the consumer into an email drip campaign, but more advanced merchants can use the consumer app to engage with various in-store personas on a basis of frequency or role in the buying organization. For example, you would treat a regular differently than a first-time customer, or a check writer versus a user in an organization. All of this context can be contained within your app.

It also allows for a deeper level of engagement during the check-out process. You’ll already have seen some version of this in your own transactions—merchants encourage consumers to subscribe to their loyalty programs, cross-promote other products, or ask for a review of their service. All of this is possible with a VSV consumer app wedge.

Improve the Experience

Merchants can use the consumer app to offer customized service, recommendations, and general consumer education. Throughout the consumer’s interaction with the merchant, a VSV consumer wedge acts like greased butter, smoothing the transaction out with features like self-serve. All of these are enabled by being integrated with the VSV platform, making it a clear win for its merchants.

Drive Demand

Perhaps the biggest value for the consumer app is that it can start to funnel demand. Most VSVs are only present at the end of the purchase consideration funnel, facilitating the transaction. A consumer app allows a VSV to move up the funnel, increasing their importance to the merchant: marketing campaigns can turn one-time customers into repeat purchasers, social hooks with group functionalities like “order together” can attract new customers, or it can be as simple as embedding an Instagram share button to drive general awareness.

Defensive Bulwark

Finally, and perhaps most importantly, a consumer app serves as a shield to fend off marketplace competitors seeking to disrupt your business. Dislodging a VSV is hard enough for a marketplace competitor, but it’s damn near impossible if the VSV has a control point with both the merchant and a direct relationship with the merchant’s consumer.

I won’t sugarcoat this—it will not be an initial easy sell to merchants. It is crucial you build processes to soothe merchant concerns when you launch a consumer wedge.

Overcoming Merchant Objections

Most merchants are naturally suspicious of anything coming between them and their consumers. Their biggest fear is that a VSV consumer offering will put their customers at risk of being stolen by other merchants. These suspicions can lead to objections that end a VSV’s consumer effort before it can even get started.

Slice overcame these concerns by deeply understanding the nuances of their vertical. In my interview with the founder, Ilir Sela, he told me that

“Having grown up in the pizza industry, I know that there’s an existing community that already lives in the pizza category. A lot of owners are separated by just one or two degrees. If I own a pizza shop, so does my brother, and so does our first cousin and her uncle, and so on and so forth. …while there’s respectful competition, most pizza shops don’t necessarily view each other with these incredibly competitive dynamics. …the vast majority of the pizza space is in the suburbs, and these locations are incredibly connected already. It just happens to be offline.”

While you may not be so blessed as to have merchant’s that are all blood relatives, there are concrete, strategic reasons for merchants to use your app. Sela said it best:

“Our product isn’t really designed to change the customer’s behavior; our product is about amplifying the existing behavior. Whether we like it or not, the consumer is already ordering from three or four other locations. They just happen to do it either on the phone or, maybe, these days, using one of these third-party delivery marketplaces. …The same economics exist whether the customer is ordering through a website of the pizza shop or from the Slice app. Different pizza shops don’t pay different economics for incremental demand. Our job isn’t to move a customer from one shop to the other; it’s to connect them with their local favorites.”

A consumer app is almost always cheaper than using a marketplace with exorbitant take rates. Your app will be a welcome alternative.

In general, to overcome these objections, a VSV needs to make the case for why a VSV consumer app can actually be highly valuable for everyone involved. We’ve found a few key talking points can help diffuse the tension around the potential threat of a consumer VSV app:

- The goal of the consumer app is not to nudge a consumer to switch from merchant to merchant, but to strengthen existing merchant relationships and reiterate purchase behavior.

- A consumer app has many benefits to a merchant, but those benefits only exist if a consumer engages. A consumer app is about engagement, not discovery. Unless a merchant has significant market share, a consumer is less likely to engage with an app that is exclusive to a single merchant.

- Most consumers already engage with multiple merchants! It is unlikely that an SMB has a monopoly.

- A consumer app is a win-win model. VSVs can tell their merchants that the platform only makes money when they do via a revenue share model. “We only get paid when you do, so we want you making as much money as possible” is an argument everyone likes.

Assuming you can get all necessary parties interested, the best place to start is with an app targeted towards individual needs.

Individual Utility Wedge

It is notoriously difficult to break through and capture a consumer’s attention. Even something as simple as getting a consumer to download an app or fill out a registration form is challenging. To build this product you have to execute at the highest level—individuals are besieged by companies trying to get their time, so creating an interface that works is crucial.

Perhaps counterintuitively, it isn’t necessary to start out by building out an app. A QR code pointing to a mobile site will get the customer on your brand journey just fine. If you’ve built a magical experience and have sufficient merchant density, consumers will naturally start to prefer your technology and proactively seek out your app on their own.

So where should a VSV begin to build a magical experience?

The Merchants are Key

Start with what you’ve got! Consumers want to interact with the VSV’s merchants. You can use that point of engagement to build a consumer experience.

Focus on High Utility

It sounds obvious, but the winning move is to focus on and improve the most frequent or important interactions between a merchant and their customer.

Replace Human Assistance with Digital Delight

Find places where you can automate away annoying moments for consumers. For example, CCC gets rid of the painful discussion with agents right after a crash by offering a photo analytics app. Additional arbitrage can exist by a company abstracting away regulatory complexity. Dutchie Pay (Disclosure: I’m a proud investor) does this for their cannabis merchants. Most cannabis shops are only able to accept cash because of federal guidelines—Dutchie Pay handles the regulatory back end and banking compliance to allow their merchants to accept credit cards.

Going Full-Featured Consumer

If you’ve landed that consumer wedge with a high utility, there are a few nuances to consider for building a fully-featured, magical consumer experience.

Personalizations

Data can greatly enrich the consumer experience, particularly if that consumer engages with the merchant or category frequently. You can use that data for recommendations, surfacing order history to generate order-again prompts, auto-filling personal preferences, and filling in loyalty info.

Unique Content

The more targeted you can make the consumer marketing, and the more exclusive you can make the information you are sharing with them, the higher the app’s utility. Whether the data you input is the merchant profile (hours of operations, locations, accessibility), inventory levels (menus, room rates, and good availability), or even just employee info, all of these inputs can increase conversion rates.

Communication

Facilitating merchant-to-consumer communications is a natural opportunity for VSVs. Digital communications have the advantage of speed, privacy, and convenience—the VSV can be the facilitator of these interactions.

Digital communication tools become even more crucial when they involve multiple parties. Complex tasks such as food manufacturing may require intense collaboration across multiple specialized vendors. For example, something as simple as a cup of yogurt will require product information input from ingredient producers, the CPG merchant, regulatory bodies, retailers, and the instore service provider. A VSV can serve to centralize, coordinate, and collaborate multiple parties across fragmented value chains or complex tasks. In doing so, they become an interface point to the consumer and an industry control point.

Magical consumer experience? What the heck am I waxing on about? Truth be told, I ripped the phrase off from my old boss Jay Hoag…he couldn’t explain it, either. But like the old saying about pornography goes—you know it when you see it.

A magical consumer experience is a step function increase in the utility curve. Think the classic consumer value framework:

Convenience: The Uber analogy was your phone as a remote control. Press a button and a car just shows up.

Price: Early days of Groupon—everything ½ off!

Selection: Amazon—the Everything store

Quality: Tiffany’s—does anyone really know if one diamond is more flawless than the next?

Risk: Consumers hate risk. Whether that is the risk of fees (Netflix original DVD business=no more rental shop fees), the risk of paying too much (Hopper=Don’t worry about the price of your flight dropping) or the risk of paying for a fake (eBay authenticity guarantee for luxury goods).

Integration to Third-Party Payers or Lenders

For more complex transactions, having pre-approved partners and payment methods can make a big difference. For inspiration in consumer, you can look to examples like CCC repair shops being pre-approved by auto insurance. In healthcare, Growth Therapy has their therapists pre-approved by health insurance. Access to credit can be a differentiator for VSVs like ServiceTitan, which offers credit their merchants can extend to their end customers for equipment leasing.

Creating Demand with a Consumer App

Once you’ve created direct consumer engagement surfaces, utility wedges, and the full-feature apps we’ve already discussed, what’s the payoff in terms of driving demand? We’ve seen consumer apps drive demand in two ways: 1) creating virality through group utility and 2) moving consumer engagement up and down the funnel.

Individual Utility → Group Utility

Your consumer app gives you a relationship with consumers. The big question becomes whether you can leverage that relationship with an individual to attract additional consumers for you and your merchants. Admittedly, this idea is more of an ambition than a proven playbook in western cultures. However, it is an idea worth pursuing—companies in China give hints on how it could work.

The core growth loop in Chinese group utility apps are team buys, where groups of people purchase goods together. Pinduoduo had 10M users just one month after it launched its first-party app, and over 500M active buyers within four years. This is especially impressive compared to the ~15 years it took Alibaba to reach that mark.

Pinduoduo triggered community buys by increasing merchant discounts with higher volumes of goods being purchased. However, price doesn’t always have to be the only incentive. You should think through unique offerings that can be triggered by group buying. Merchants may be willing to offer exclusive products, unlocked by groups above a certain size. Local density can also allow for bundling offerings across merchants within a category (such as in pizza and ice cream delivery) or across categories (ticket to a game, nearby restaurant reservation). You already have the merchants on your software, so take advantage of the power of that digital automation!

Moving Consumer Engagement Up and Down the Funnel

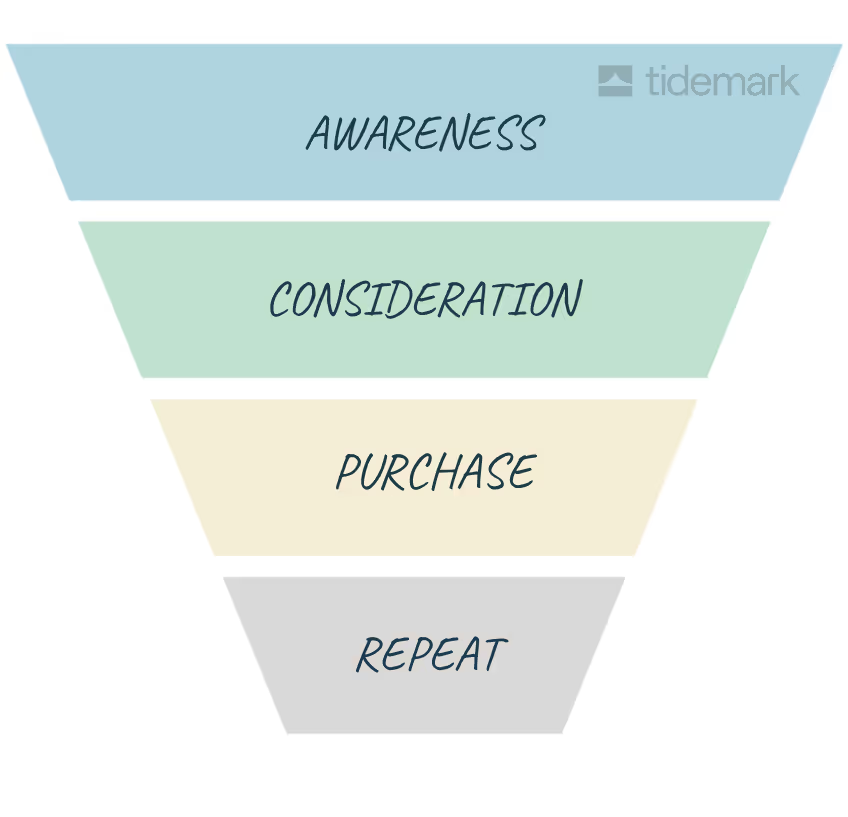

You can think of a consumer’s journey as a funnel:

Typically, a VSV is engaging with consumers who are in the transaction stage and are ready to buy. It can help merchants increase the conversion, cart size, etc. (see Part 2), but the VSV is not attracting new customers to the merchant or increasing the engagement frequency of existing customers. To do so, you’ll want to deploy strategies to move up and down the consumer funnel.

Repeat: The easiest move is to encourage repeat purchase behavior. Building one-click order again, favorites, and recommendations based on previous purchases can allow a VSV to increase ARPU for the merchant’s customers.

Consideration: This is the first dramatic move up the funnel. Consideration is where a consumer knows they want a product, but may not know which brand/merchant they want it from. A VSV can offer guidance through the recommendations of a friend or community reviews. The consumer app will ask for review in key parts of the consumer journey and then publish that review to third-party review aggregators. After each dining experience booked on its platform, OpenTable prompts customers to submit reviews, which are then shown to other potential diners when they are searching for a reservation. When a Yelp customer submits a request for a quote from a plumber, Yelp will offer to send the same request to other plumbers in the area. Through "personalization" at the point of sale like Toast and ecommerce like Dutchie, VSVs can recommend third party products and charge ad-like take rates for it.

Awareness: This is the most difficult but most valuable stage. Here, a VSV’s role is to make consumers aware of a good and a merchant. This can occur through consumers raving about the merchant, product, or experience on social media. Alternatively, they can come into contact with the merchant through group engagement mechanisms like I described above (group buys or reservations).

TripAdvisor is a good example of this stage in the funnel. TripAdvisor CEO Steve Kaufer characterizes their design as “very up-funnel”, allowing users to see reviews of Facebook friends and follow favorite influencers for travel tips and inspiration, well before they are planning a trip. As TripAdvisor becomes a source of travel inspiration, hotels and other travel merchants have an opportunity to build awareness and influence decisions much earlier in the travel journey. Start thinking in downloads, MAUs, DAUs, and pageviews in addition to ARR, locations, and ARPU.

Conclusion

By extending with a consumer application, you’ll help your merchants get closer to creating demand and reduce the threat of the other demand aggregators moving towards your market. In Part 4, I will discuss the most lucrative and most speculative portion of this strategy: launching your own marketplace.

Consumer Demand Series

Introduction

Part 1: Merchant Front Office Apps - Setting the Foundation

Part 2: Creating Demand with Merchant Facing Apps

Part 3: Consumer Apps

Part 4: The Big Leap to Two-Sided Marketplace

CASE STUDIES RELATING TO THIS CHAPTER:

SiteMinder: Extending into Consumer Demand

Win

Extend

Case Studies

New to the VSKP?

Get the VSKP delivered to your inbox. Each week, we'll send one strategy essay along with related case studies to help you make sense of it all.

Sign up for VSKP weekly deliveryKeep up with the VSKP

"The Vertical SaaS Knowledge Project" — Sign up to receive new content as soon as it's released.